April 14, 2016

June 28, 2014

TradingVolatility.net for $VIX

TradingVolatility.net, great for $VIX, $VXX and volatility tracking.

May 12, 2013

Option pit

Optionpit blog seeks volatility for options traders.

May 7, 2013

Vix Central

Vixcentral is a great dashboard for volatility trading.

April 1, 2013

Tradelog Software for tax preparation

Tradelog Software does all the obvious things for traders' taxes; which is nice, because the IRS does not.

Broker 1099-B reports are often useless for tax reporting since the IRS has different rules for taxpayers than they do for brokerages. No, you did not read that wrong! Let me say that again: The IRS has different reporting rules for taxpayers than they do for brokerage 1099s. And in many cases (maybe as high as 90%) your brokerage 1099-B will not match with what you, the taxpayer, are required to report on Schedule D Form 8949.

Greene recommends it:

We frequently find errors in other programs and solutions on wash sales, tax treatment and more. Many of these programs or solutions are geared toward the needs of brokerage firms, and IRS rules for broker-issued securities 1099-Bs are materially different from what taxpayers need to report on their Form 8949/Schedule D. Brokers are permitted to report potential wash sales based on "identical positions," whereas taxpayers must report actual wash sales based on "substantially identical positions" (between stocks and stock options based on the same symbol). Many tax preparers get lazy and import broker-issued securities 1099-Bs into their tax preparation software which is a huge mistake, because it will either overstate or understate trading gains and losses

May 12, 2012

Position: open to enter, exit to close

Four things to understand before adding risk via options:

1. Understand the Cause of Volatility in your instrument

2. What is ATM Implied Volatility

3. What is the Curvature of the Skew (how pricy are calls and puts)

4. What is the current Term Structure

-- OptionPit

May 7, 2012

VXX loses

Roll Yields'

That issue isn't disclosed until page 15 of the note's prospectus: "The existence of contango in the futures markets could result in negative 'roll yields', which could adversely affect the value of the index underlying your ETNs and, accordingly, decrease the payment you receive at maturity or upon redemption."

Kristin Friel, a spokeswoman for London-based Barclays, declined to comment.

The average ETN annual investor fee is 0.84 percent, according to Morningstar data. That doesn't include a lot of the tacked-on charges, Lee said. The UBS short VIX ETNs, for example, add about a 4 percent annual fee for "event-risk" hedging, leading to a total cost of 5.35 percent, he said.

Christiaan Brakman, a UBS spokesman, declined to comment.

April 25, 2012

Billl Luby trades the VIX

focused on buying some of the inverse VIX ETPs, notably XIV and SVXY, when they saw the VIX spike. Some have preferred shorting VXX, TVIX and UVXY, based partly on availability, while others have preferred to trade VXX options, generally by buying puts or limiting risk with the likes of a bear call spread.I had thought that my recent article Options on UVXY and SVXY Open Up New VIX ETP Trading Approaches might nudge some traders into considering strategies involving the +2x leveraged long VIX short-term futures ETF (UVXY) and perhaps utilize the -1x short VIX short-term futures ETF (SVXY) as well, but based on the volumes, these issues are still in the process of gaining a broader audience. In fact, UVXY did see record call volume of 7,300 contracts on Tuesday, but SVXY has been the laggard so far, as the graphic below illustrates.

So here is a thought: The next time the VIX has a significant spike, one of the first trades you should investigate is fading that spike by buying SVXY out-of-the-money calls. This is a simple trade and has the potential to be quite profitable. The SVXY April 90 calls, for instance, have jumped 40% from Tuesday's close.

The exciting news about options on SVXY and UVXY is that traders can now easily structure a broad variety of trades that involve defined risk and substantial upside. While VXX (and VIX) options are still the gold standard in terms of liquidity, SVXY and UVXY options also deserve some love - even if the spreads are still wider than those of VXX.

April 23, 2012

$VXX goes down 80 percent of time

"Everyone knows" that US residential real estate is a bad investment, with the Case Shiller Home Price Index having dropped by about 32 per cent since its 2005 peak. At the end of last week, the iPath S&P 500 Vix Short Term Futures Exchange Traded Note had lost that much in one month. Not seven years. One month. Over the previous six months, the vehicle had lost more than 69 per cent of its value. The managers didn't do anything other than rigorously follow their charter, and their strategy has been fully disclosed, along with the trading history.

The reaction of some investors to this record is interesting: they have been doubling down. There has been a spurt of option buying on the ProShares Ultra Vix Short Term Futures Fund, which aims for twice the daily return for the Short Term Vix Futures Index.

Vix futures or options, you are not actually buying "volatility". Those products are based on the prices of forward start variance swaps. If you don't know what that means, don't buy Vix products.

January 10, 2012

Inverse volatility: XIV, not VIX

VelocityShares Inverse VIX ETN (XIV)

This ETN offers daily inverse exposure to an index comprised of investments in short-term VIX futures contracts-a strategy that has struggled mightily in 2011 thanks to heightened volatility and backwardated markets. Though XIV has lost more than 40% of its value in 2011, there is reason to be optimistic that at least the beginning of 2012 will be more favorable. The VIX, a measure of expected equity market volatility, has declined considerably in recent weeks as optimism over the global economy has returned. And more importantly for XIV, contango in VIX futures markets has also returned; the futures curve now has a steep upward slope, a condition that can give a nice boost to the strategy employed by XIV [see also Low Volatility ETFs Attracting Big Inflows].

Given that XIV utilizes a futures-based strategy to deliver inverse exposure, this ETN probably isn't appropriate for risk-averse investors who aren't willing or able to regularly monitor their positions. But for those who grasp the complexities associated with XIV, the current environment might just be perfect for this ETN. XIV might not be a good ETN to own throughout 2012, but it certainly seems to be positioned nicely for a strong start to the year.

April 11, 2011

Buy realized volatility, sell implied volatility ?

Unlike 2008 and 2010 implied volatility the market over estimated implied volatility going into and out of the Japan crisis -- why then should Vix be trading so low now?

Vix parity, volatility arbitrage and Japan

Posted by Izabella Kaminska on Mar 29

February 12, 2011

Options expiry 2011

Options expiry 2011 by month: Month: Expiry, Trading Stops and Settlement Occurs

January: 21, 22.

February: 18, 19.

March: 18, 19.

April: 15, 16.

May: 20, 21.

June: 17, 18.

July: 15, 16.

August: 19, 20.

September: 20, 21.

October: 21, 22.

November: 18, 19.

December: 16, 17.

January 14, 2011

Implied volatility vs historical volatility

I mean if you knew in advance that historical volatility will sit at 5 for the next month, then yes, selling SPY options at 15 volatility sounds like a great idea. The point is though one looks backward (HV) and the other estimates forward (IV). An HV of 5 is unsustainably low, it suggest 2/3 of all days will see a .3% range or less in SPY. The HV numbers we see now look back at an incredibly non-volatile holiday stretch. Options rightly price in that we won't see that kind of non-action going forward.

For an extreme example of how HV and IV can diverge, consider a small binary-ish biotech ahead of news on some product. The stock itself may have tiny volatility, while options price in that the stock will double or halve once the news comes out. The attached graph shows DNDN over the past year, 20 day HV vs. 30 day IV. In late April ahead of news, IV sat at 140, HV at 30. After the news and the 30% gap, HV shot up to 110, and IV plunged to 60. The news was out. And no one would suggest options were a major buy at 60 volatility, other than a bot that would pick them up as cheap vs. historical volatility.

-- Adam / Daily

May 20, 2010

The options Insider

theoptionsinsider looks at options trading strategies.

August 15, 2009

Consolidated financial planning

mystockoptions includes stock options in financial planning.

December 16, 2008

Greeks of leveraged ETFs

Ultra ETFs deliver a 2 delta. There is a negligible amount of gamma, theta, and vega, a small amount of rho, and some exposure to dividend risk and borrowing costs.

-- ET comment on the option greeks of ETFs.

October 10, 2008

Think or swim: think different than other brokers ?

Think or Swim aims for high volume from quickly expiring options.

The average accounts remain above 40K. The Annual avg trades per remain

above 180 and the churn hovers around 7%. TOS is pillaging competitors at

a 14:1 ratio (nearly 12,000 accounts taken away from OXPS, Schwab, TD,

Etrade etc in 6 months).

Continue reading "Think or swim: think different than other brokers ?" »

September 8, 2008

Option Volatility & Pricing: Advanced Trading Strategies and Techniques, Sheldon Natenberg

Option Volatility & Pricing: Advanced Trading Strategies and Techniques, second edition (1994, Hardcover) by Sheldon Natenberg.

Natenberg not only takes great pains to explain the concept of volatility, in addition to other inputs into an option pricing model, but clearly shows that option pricing isn't the exact science many seem to believe, for the simple reason that we never know if our volatility estimate is correct.

September 6, 2008

Options as a Strategic Investment, Lawrence G. McMillan

Options as a Strategic Investment, 4th Edition (2001), by Lawrence G. McMillan .

Comprehensive and informative. Covers pretty much every conceivable option strategy in the context of both equity and futures options and imparts realistic expectations.

August 16, 2008

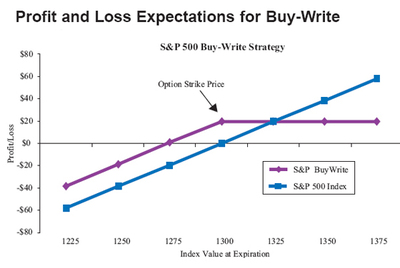

Buy-Write covered calls: BEP and BWV

There are many funds today offering some version of covered call strategy (BuyWrite strategy). We have been asked "What do they do?" and "Are they a good addition to a diversified and allocated portfolio?"

In September 2004 the Ibbotson Associates consulting found higher returns and much lower volatility for a the BuyWrite index versus the S&P 500 alone.

-- qvmgroup

August 6, 2008

Etrade options

August 1, 2008

Optionetics

Optionetics pitches options trading to retail investors. Will training make informed investors ?