Buy-Write covered calls: BEP and BWV

There are many funds today offering some version of covered call strategy (BuyWrite strategy). We have been asked "What do they do?" and "Are they a good addition to a diversified and allocated portfolio?"

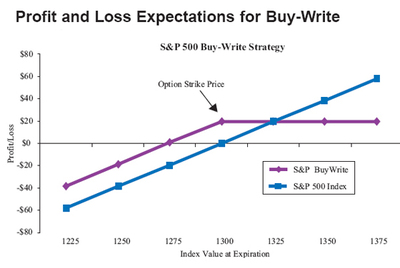

In September 2004 the Ibbotson Associates consulting found higher returns and much lower volatility for a the BuyWrite index versus the S&P 500 alone.

-- qvmgroup

Fund descriptions from the sponsor's sites:

BEP: The Fund's investment objective is to seek total returns through a covered call strategy that seeks to approximate the performance, less fees and expenses, of the CBOE S&P 500 BuyWrite. The Fund will pursue its investment objective principally through a two-part strategy. First, the Fund will invest the proceeds in all of the common stocks included in the S&P 500 Index weighted in the same proportions as the S&P 500 Index and/or other investments that have economic characteristics similar to the securities that comprise that Index. Second, each calendar month during the term of the Fund, the Fund will write (sell) one-month call options on the S&P 500 Index ("Written Options").

BWV: iPath Exchange Traded Notes (ETNs) are senior, unsubordinated, unsecured debt securities issued by Barclays Bank PLC delivering exposure to the returns of a market or strategy with the trading flexibility of an equity. Investors can trade iPath ETNs on an exchange at market price or receive a cash payment at the scheduled maturity or at early redemption, based on the performance of the index, less investor fees. The iPath CBOE S&P 500 BuyWrite Index ETN offers investors cost-effective and tax-efficient exposure to the CBOE S&P 500 BuyWrite Index, commonly known as the BXM Index (the "Index"). The Index is designed to measure the total rate of return of a hypothetical "buy-write", or "covered call", strategy on the S&P 500 Index. This strategy consists of a hypothetical portfolio consisting of a "long" position indexed to the S&P 500 Index (i.e. purchasing the common stocks included in the S&P 500 Index) and the sale of a succession of one-month, at- or slightly out-of-the-money S&P 500 Index call options that are listed on the Chicago Board Options Exchange ("CBOE").