« March 2013 | Main | May 2013 »

April 29, 2013

April 28, 2013

Understanding of Information Uncertainty and the Cost of Capital

Uncertainty and the Oil Fields

The reason for the review is that an Australian scholar has recently published a paper offering "A Bayesian Understanding of Information Uncertainty and the Cost of Capital." The gist of it is that traders face information uncertainty, that is, the risk of a misleading signal about the value of an asset.

"The Bayesian position," says D.J. Johnstone of the University of Sydney Business School, "is that even a highly informative signal ... can bring an increase in uncertainty, and hence an increase in the cost of capital." This is at least somewhat counter-intuitive. Surely the highly informative signals (also known as "greater transparency") will lessen uncertainty and risk, thus reducing the cost of capital.

Ah, Johnstone says, perhaps not. Consider a world in which there are two possible geological formations involved in the search for oil: A and B. There may be oil under either plot. Geologists tell us that plot A belongs to a type of geological formation with a 0.5 frequency of oil. B-type plots, on the other hand, have a 0.95 frequency of oil. It isn't always obvious which is which, and oil companies like to figure out which is which before making the final decisive test to determine whether there is oil there.

Suppose also that the prior probability of oil under a random site, before we even know if the site is A or B, is 0.635.

Now, on Day 1, an oil company owns a piece of land that has not yet been tested for oil, or even tested to determine whether it is A or B. The market will presumably assess the value of this land accordingly. Prospective buyers will consider it as having a 0.635 likelihood of bearing oil.

On Day 2, the land is tested and found to be of Type A.

Thereafter, the market will lower the value of that land, because its likelihood of bearing oil has fallen to 0.5. There is greater uncertainty post-test than there was pre-test.

A Bayesian Understanding of Information Uncertainty and the Cost of Capital

David James Johnstone

University of Sydney - Discipline of Finance

January 1, 2013

Abstract:

The term "information risk" or "information uncertainty" is defined as the risk of a misleading signal. This risk is understood Bayesianly in terms of the likelihood function f(S|φ). In Bayesian method, f(S|φ) captures the quality of signal S with respect to parameter φ. The Bayesian position is that even a highly informative signal (one with a very peaked likelihood function) can bring an increase in uncertainty, and hence an increase in the cost of capital. It can also occur that the cost of capital implied by a capital asset pricing model (CAPM) increases even when better information brings greater certainty. The role of financial reporting should be understood not in terms of its effect on the cost of capital per se, but as aiding investors to assess the probability distributions of future cash flows more accurately, thereby leading on average to higher expected utility portfolios. This is a technical version of the traditional view in accounting theory that financial disclosure should provide generally relevant information for asset valuation and other investment decisions.

April 27, 2013

State of Bank Regulation

In 2011, Jamie Dimon, chief executive of JPMorgan Chase, said that the proposed rules to overhaul derivatives, a commonly used financial instrument, "would damage America." He also said that the Basel rules were "anti-American." Comment letters filed by lobbyists with regulators used sophisticated-looking models to show how rules could hold back the economy.

"As far as the banks are concerned, there is never a good time to raise capital or increase regulation," Ms. Bair said. "When times are bad, they say it could hurt things, and when times are good, they say they don't need it."

Some analysts, however, caution against reading too much into the banks' strong profits.

Though banks have been preparing for new rules for months, many of them have not been fully executed, which means the true costs of the measures will not be known until later.

Dick Bove, a bank analyst at Rafferty Capital Markets says that, while bank profits have hardly suffered from new regulation, their customers have. Lenders have simply passed on many of the costs, mostly in the form of new fees, he said. "The government aimed a Stinger missile at the banking industry and missed and hit the consumer instead," said Mr. Bove, who also notes that loans to small business are still weak.

In addition, bank profits may not be as strong as they look, say some analysts. Earnings appear less impressive when taking into account the new capital that banks have to hold. This can be seen when applying a metric called return on equity, which reflects the extra capital.

Financial companies in the Standard & Poor's 500-stock index had a 7.9 percent return on equity last year, according to data from S.& P. That's below the 10 percent return for utilities last year, also a regulated industry. And the banks' return is down from the 16 percent return that they achieved in 2006.

April 26, 2013

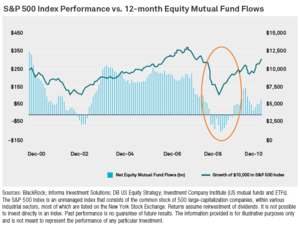

Buy low, sell high: hard to execute

BlackRock overlays the performance of the S&P 500 with equity mutual fund flows.

"Unfortunately, investors often take actions counterintuitive to investing best practices," they write. "In an ideal world, investors 'buy low, sell high.' Though the rule seems simple, we've often seen investors do the exact opposite, especially during volatile times."

April 24, 2013

Experiment design: psychology

Diederik Stapel, a Dutch social psychologist was approached by another colleague of his at Tilburg, Ad Vingerhoets, who asked Stapel to help him design a study to understand whether exposure to someone crying affects empathy. Stapel came up with what Vingerhoets told me was an "excellent idea." They would give elementary-school children a coloring task in which half the kids would be asked to color an inexpressive cartoon character, while the other half would have to color the same character shown shedding a tear. Upon completing the task, the children would receive candy and then be asked if they were willing to share the candy with other children -- a measure of pro-social behavior.

April 23, 2013

saving old buildings and neighborhoods is essential to the continued vitality of great cities

In the early 1990s, Shanghai organized a special economic zone that led to the development of a financial hub in Pudong, on land previously occupied by warehouses and wharves. Towers sprouted to create an instant iconic skyline, but with a regrettable, scaleless urban moonscape below.

Should we in New York in 2013 emulate the Shanghai of the 1990s? Or should we heed the lesson the Chinese themselves have subsequently learned, that saving old buildings and neighborhoods is essential to the continued vitality of great cities? In Shanghai, the pre-World War II buildings along the Bund, which loom so very large in the city's appeal, have been saved and repurposed. Nearby, at Xintiandi, a historic residential neighborhood of stone houses and tight alleys has been transformed into a chic, walkable retail and entertainment district.

Terminal City, a sophisticated mix of hotels, clubs, office buildings and residential blocks at the heart of East Midtown, was built on platforms bridging the rail yards north of Grand Central. It was a bold plan to create valuable real estate where once there had been urban blight. As much as anything, this development created what the world knows today as Midtown Manhattan.

-- Robert A. M. Stern

SoHo and the Flatiron district were two of the most moribund parts of the city in the 1960s and '70s; once they were designated as historic districts, the fortunes that poured in made them more vital than ever.

We can do the same in East Midtown. The historic hotels and older office buildings of Terminal City could be repurposed for residential uses (and, I might add, the Yale Club is doing just fine). Some of these older buildings, their futures uncertain, may look a little dowdy today, but I'm confident that the stability that landmark designation provides would lead owners and developers to rediscover their intrinsic value.

Our diversity, and the fact that we don't look like Pudong, is the reason many creative types choose New York over the bland banalities of Silicon Valley, just as in London, they've chosen Clerkenwell over Canary Wharf, and in Paris, just about anywhere over La Défense.

April 16, 2013

Quant Start Quantitative-Finance-Reading-List

List by Michael Halls-Moore of Quantstart.com:

General Quant Finance Reading (Michael Lewis, Roger Lowenstein, Emanuel Derman).

Interview Preparation (Paul Wilmott, Mark Joshi)

Quantitative Trading ( Sheldon Natenberg, Nassim Nicholas Taleb, Barry Johnson, Euan Sinclair)

Mathematical Finance / financial engineering (John Hull, Salih Neftci)

Interest Rate Derivatives (Damiano Brigo, Fabio Mercurio)

C++ (Scott Meyers )

Python (Mark Lutz)

MATLAB ( Paolo Brandimarte)

R (Phil Spector, Norman Matloff, Paul Murrell)

Excel/VBA (Fabrice Douglas Rouah, Gregory Vainberg)

Quantstart's Quantitative-Finance-Reading-List

Pavel Tsatsouline -The seminar on kettlebell stretching

Pavel Tsatsouline -The seminar on stretching for kettlebell training.

April 15, 2013

Agency Shortcut mortgages

Michael McCoy, a SunTrust spokesman, declined to comment on the whistle-blower's allegations, saying the bank was unaware of the complaint. He said in a statement that the bank's policy was to use Fannie's and Freddie's guidelines when underwriting mortgages that would be sold to them. Nevertheless, the complaint details how it says some SunTrust mortgage sales representatives manipulated an automated loan underwriting system to gain Fannie's and Freddie's approval for mortgages that did not meet those companies' standards. These loans, sold mostly to Fannie, were called Agency Shortcut mortgages.

¶ SunTrust sales representatives entered fabricated income and asset figures into the bank's exclusive version of Fannie Mae's Desktop Underwriting system, the complaint says. Fake numbers, it says, would generate automatic approvals for unqualified borrowers, "at the same time preventing underwriters from exercising proper oversight."

¶ That oversight was thwarted because once the system's approvals kicked in, the complaint contends, underwriters in SunTrust's due diligence department could not stop the loans from being sold to Fannie or Freddie. There was no turning off the assembly line.

¶ The complaint contains several internal SunTrust documents to support its allegations. One is a promotional piece for sales reps that explains the Agency Shortcut mortgage. "It's a SISA (Stated Income/Stated Asset) at full doc pricing," it says. Translation: undocumented loans carried the same interest rate as a fully documented version.

Because of fabrications, the complaint says, Fannie Mae's system recognized these loans as fully documented. But according to the complaint, the Agency Shortcut mortgage waived property inspections and did not require the borrower to sign the document that allows the Internal Revenue Service to provide a prospective lender with a borrower's income. In addition, borrowers of these loans could have a debt-to-income ratio of up to 64.99 percent, an onerous level.

¶ SunTrust terminated the Agency Shortcut program in April 2008, the complaint says. Two months before, Fannie Mae limited the number of times a sales rep could enter information on a single borrower, according to the complaint. This might have been in recognition that its underwriting system was being gamed by repeated efforts to gain a loan approval.

¶ The complaint contends that SunTrust originated "tens of billions of dollars" in Agency Shortcut mortgages. It is unclear how many of these loans landed at Fannie or Freddie; Suntrust's financial filings say the bank sold $98.6 billion in total loans to Fannie and Freddie during the three years ended 2008.

¶ Support for the whistle-blower's descriptions of lax lending at SunTrust seems apparent from the boatload of loans sold to Fannie and Freddie during the mortgage mania that the bank has had to buy back. Such repurchases are typically done with loans that failed to meet standards -- like borrower quality -- or other characteristics promised to the purchasers at the time of the sale.

¶ Over the last three calendar years, according to its financial statements, SunTrust has repurchased $2.235 billion of mortgages, the bulk from Fannie. Fannie requests these repurchases, and documents show that Suntrust's constituted the fifth-largest amount among lenders at the end of 2012. It ranked not far below the much larger JPMorgan Chase.

¶ And at the end of 2012, SunTrust said it had $655 million in repurchase requests outstanding. Mr. McCoy, the spokesman, said the bank's buybacks reflected its heavy concentration of lending in Georgia and Florida during the bubble.

¶ "We sold a higher percentage of loans to Fannie Mae than did some of our competitors," he said, "so it also stands to reason that our demands from Fannie Mae could be higher than some peers." The loan types that included the Agency Shortcut have accounted for just 20 percent of the bank's buybacks, he said.

April 14, 2013

Quicken Loans a $100 billion mortgage business, the third-largest home lender in the country, behind Wells Fargo and JPMorgan Chase -- Mortgage Daily

WHEN Dan Gilbert was in the fourth grade, he bought candy at wholesale from the father of a friend and sold it at retail prices to classmates. It was the start of a nearly obsessive quest to create enterprises and earn profits. He estimates that he's either invested in or started 70 companies in his career. One early and ill-fated venture was running a short-lived bookmaking operation with some friends while a freshman at Michigan State University. It ended when he was arrested by an undercover agent. He served probation, the charges were dropped and there was no conviction.

"We were college teenagers," he said.

Subsequent ventures were more mundane, and far more successful. He later earned a real estate agent's license and, while at Wayne State University Law School, worked part time at a Century 21 office. At some point, he realized that the serious money was in selling mortgages, not homes. So he and two partners, including his younger brother, Gary, went into the mortgage-origination business together. Mr. Gilbert and his partners took out ads in those once-ubiquitous free magazines that listed houses for sale, something that none of his competitors did.

"From the very beginning we could make the phones ring," Mr. Gilbert said, "even if we didn't know what to do once they rang."

The company, called Rock Financial because it sounded sturdy, would eventually become Internet-based, selling mortgages in all 50 states. It was acquired by Intuit for $532 million in 1999, says Mr. Gilbert, and renamed Quicken Loans. Three years later, after the dot-com bubble burst, the company was sold to a group of investors led by Mr. Gilbert for a sum he put at roughly $55 million.

This year, Quicken Loans will do $100 billion worth of mortgage business, says Mr. Gilbert, making it the third-largest home lender in the country, behind Wells Fargo and JPMorgan Chase, according to Mortgage Daily.

Quicken Loans now employs nearly 2,500 mortgage bankers. One morning last month, 300 of them were working on the third floor of the Chase Tower, and a swing through the office was like a visit to a frat party at a telemarketing firm. There were many men and some women with headsets, talking to customers and staring at computer screens -- nothing novel there. But a karaoke machine sat in an aisle. Guys threw footballs to one another; one employee shot at colleagues with a Nerf gun. Basketball pennants were draped from the ceiling, as part of a March Madness theme.

"You should have been here last week," said one broker, Nerf gun in hand. "The theme was spring break. I was wearing shorts, a hat, sunglasses."

Mr. Gilbert espouses a philosophy of instilling fun in the workplace, one piece of an elaborate corporate culture that he has fine-tuned over the years, and describes, every few months, in a surprisingly entertaining, seven-hour monologue to new employees. One of more than a dozen core principles described in "Isms in Action," as the lecture is titled, is summed up as "Obsessed with finding a better way."

April 13, 2013

Co-ops rent some units for the benefit of all

A lucrative ground-floor lease can add 10 percent or more to the value of an apartment, residential brokers say. A sprawling two-bedroom loft at 464 Broome Street in SoHo, New York, for example, is in contract for $3.22 million, nearly 10 percent over its asking price, in large part because the listing not only offers no maintenance but provides its shareholders with $20,000 a year in income.

"The building has just eight apartments," said Henry Hershkowitz, a broker at Douglas Elliman who represented the seller, "so the revenues from the two stores on the ground floor cover the real estate taxes, the building's upkeep, even a full-time super, and then there is money left over for an annual dividend."

An apartment of this size in SoHo would typically come with a monthly maintenance of $2,400, said Robert Dankner, the president of Prime Manhattan Residential, which represented the buyer. When $20,000 a year in dividends is added to the nearly $30,000 saved in maintenance, there is a net savings of close to $50,000 a year, he noted.

As Mr. Dankner put it: "Depending on how you model it, it would take $750,000 earning a 6.5 percent interest to get that kind of return. Or, if they live there for 10 years, they save themselves half a million dollars. If you think of it from this perspective, even with the bidding war and it selling for over ask, the apartment was undervalued."

Others that decided not to sell their retail circumvented the 80-20 rule by creating a long-term master lease of the ground-floor space, in which the owners of the master lease would be all building residents and some outside investors, who then would sublease the space to a retail tenant at market rates. This became problematic when sellers moved out of the building but kept their ownership stake in the master lease, preventing new owners from benefiting from it.

"Now that the 80-20 rules have been relaxed," said Margaret D. Baisley, a real estate lawyer with her own practice in SoHo, "those entities who formed these master leases want to take them back, but other investors have come to own them and they don't want to change the scheme, to the detriment of the building."

And even for those buildings that own their retail spaces outright, the effect on their bottom line may be somewhat muted. "Our storefront income is great, but it is not as romantic as you may think," said Karel De Boer, an agent at Douglas Elliman and the property manager for 17 East 89th Street. "While our rent has increased, so have real estate taxes, payroll taxes and utilities."

April 12, 2013

Detroit revival

"The villains are the rules of the game," he said. "Developers find it far more profitable to build in farmland in the suburbs than in vacant land in the urban core. It's easier to acquire big sites without worrying about hidden basements, or gas stations, or a reputation for violence, or corruption or inefficiency or the potential racism of your customers."

It makes financial sense for developers, but it is disemboweling the city, he said. Which is why he believes that without reform to housing and development laws, neither Mr. Gilbert nor the emergency manager, nor any combination of earthly forces, can salvage Detroit.

Mr. Gilbert espouses a philosophy of instilling fun in the workplace, one piece of an elaborate corporate culture that he has fine-tuned over the years, and describes, every few months, in a surprisingly entertaining, seven-hour monologue to new employees. One of more than a dozen core principles described in "Isms in Action," as the lecture is titled, is summed up as "Obsessed with finding a better way."

That could work as a pretty good motto for Opportunity Detroit. It is being designed and unveiled with the city's past missteps in mind. One of the most infamous is the Renaissance Center, a huge, mirrored complex of towers built in 1977 and currently the headquarters of General Motors.

"One critic said it was the pre-eminent example of terrible urban planning," said Mr. Cullen of Rock Ventures, who formerly worked for G.M. and helped champion the idea of buying the RenCen, as everyone here calls it, and moving the company in. "The building basically sucked the remaining people out of downtown and stuck them in a fortress."

Mr. Gilbert wants to return the area to the pedestrian haven that it was decades ago. If he succeeds -- he expects significant results within four or five years -- the place will again resemble the scene captured in a photograph that is plastered on a wall not far from his office. It is a huge, sepia-toned shot of Campus Martius, snapped in 1917. Looking at the picture, you realize that it includes the neighborhood where you are standing, though at a time when it bustled with men and women in hats, strolling amid billboards, retailers and a lineup of trolley cars.

April 10, 2013

Search is more than web text, Google learns

Searches on traditional services, dominated by Google, declined 3 percent in the second half of last year after rising for years, according to comScore, and the number of searches per searcher declined 7 percent. In contrast, searches on topical sites, known as vertical search engines, climbed 8 percent.

While traditional searches increased again this year, other data reflects the threat to Google.

In the first quarter, spending on search ads fell 1 percent, a significant slowdown for Google, according to IgnitionOne, a digital marketing company. Last year, Google lost market share in search ads for the first time, according to eMarketer, falling to 72.8 percent from 74 percent.

This year, ad spending on traditional search engines is expected to grow more slowly than overall online ad spending, a reversal. Its growth significantly outpaced that of online ad spending until last year, eMarketer said.

Google is not watching from the sidelines. It is making more changes to search offerings, at a faster pace than it has in years.

Larry Page, its co-founder and chief executive, renamed the search division "knowledge." Google's mission, organizing the world's information, was too narrow. Now he wanted people to learn from Google.

Google now shows answers instead of just links if you search something like "March Madness," "weather" or even "my flight," in which case it can pull flight information from users' Gmail accounts.

The company's biggest step happened last year, when it introduced the knowledge graph. While search generally matches keywords to Web sites, the knowledge graph uses semantic search, which understands the meanings of and connections among people, places and things.

A typical search engine, for instance, responds to a search for "Diana" by showing Web pages on which that word appears, from Wikipedia entries on the goddess of the hunt and the Princess of Wales to an engagement ring company.

But a more knowledgeable, humanlike search engine could know that you were looking for your roommate Diana's online profile, or that you were also interested in Kate Middleton.

"What Google is beginning to do is share some of the knowledge in the world that humans have in their minds," said Ben Gomes, a Google fellow, "so users can begin to communicate with Google in a way that's much more natural to their thinking."

Google calls these small steps that show where it is headed.

April 9, 2013

Big data to win elections

"The trickiest problem, the one that will take the longest time to solve, is the creation of a culture of data and analytics, including training operatives to understand what data is," Lundry said. And the collaborative nature of "data ecosystems," he suggested, do not play to Republican strengths.

The Priebus report surveyed 227 Republican campaign managers, field staff, consultants, vendors and other political professionals, asking them to rank the Democrat and Republican advantages on 24 different measures using a scale ranging from plus 5 (decisive Republican edge) to minus 5 (solid Democratic advantage). "Democrats," the report noted, "were seen as having the advantage on all but one." As the graph on Page 28 of the report illustrates, most of the largest Democratic advantages relate directly to the integration of technology with "ground war" campaign activities like person-to-person voter contact, election-day turnout and demographic analysis:

The premier pro-Democratic quantitatively oriented organizations -- both for-profit and nonprofit -- have become crucial sources of data, voter contact and nanotargeting innovation for Democrats and liberal organizations. These include:

• Catalist, which maintains a "comprehensive database of voting-age Americans" for progressive organizations;

• The Analyst Institute, "a clearinghouse for evidence-based best practices in progressive voter contact," which conducts experimental, randomized testing of voter persuasion and voter mobilization programs;

• TargetSmart Communications, which develops political and technology strategies;

• American Bridge 21st Century, which conducts year-round opposition research on Republicans and conservative groups;

• The Atlas Project, which provides clients with online access to detailed political history from national to local races, including media buys and campaign finance data and a host of other politically relevant data;

• Blue State Digital, a commercial firm founded by operatives in Howard Dean's 2004 campaign that now provides digital services to clients ranging from the Obama campaign to Ford Motor Company to Google.

this Democratic advantage. Sasha Issenberg, who wrote "The Victory Lab: The Secret Science of Winning Campaigns," has described what liberals and Democrats have done to "mathematicize" voter turnout. Right after the 2012 election, Issenberg explained how things have changed:

Within the practice of politics, no shift seems more dramatic than the role reversal between the two parties on campaigning competence. Today, there is only one direction in which envy can and should be directed: Democrats have proved themselves better -- more disciplined, rigorous, serious, and forward-looking -- at nearly every aspect of the project of winning elections.

-- Alex Lundry, vice president and research director of TargetPoint, a company at the forefront of microtargeting for the Republicans in 2002 and 2004

-- Reince Priebus, chairman of the Republican National Committee

April 3, 2013

The face of pollution

Beijing: The World Health Organization has standards that judge an air-quality score above 500 to be more than 20 times the level of particulate matter in the air deemed safe. https://twitter.com/BeijingAir">twitter: @BeijingAir

Chinese officials prefer to publicly release air pollution measurements that give only levels of PM 10, although foreign health and environmental experts say PM 2.5 can be deadlier and more important to track.

There has been a growing outcry among Chinese for municipal governments to release fuller air quality data, in part because of the United States Embassy Twitter feed. As a result, Beijing began announcing PM 2.5 numbers last January. Major Chinese cities have had the equipment to track those levels, but had refused for a long time to release the data.

The existence of the embassy's machine and the @BeijingAir Twitter feed have been a diplomatic sore point for Chinese officials. In July 2009, a Chinese Foreign Ministry official, Wang Shu'ai, told American diplomats to halt the Twitter feed, saying that the data "is not only confusing but also insulting," according to a State Department cable obtained by WikiLeaks. Mr. Wang said the embassy's data could lead to "social consequences."

April 2, 2013

A rush of foreign investors into a country, followed by a sudden rush out makes for a big local financial crisis

It's hard to imagine now, but for more than three decades after World War II financial crises of the kind we've lately become so familiar with hardly ever happened. Since 1980, however, the roster has been impressive: Mexico, Brazil, Argentina and Chile in 1982. Sweden and Finland in 1991. Mexico again in 1995. Thailand, Malaysia, Indonesia and Korea in 1998. Argentina again in 2002. And, of course, the more recent run of disasters: Iceland, Ireland, Greece, Portugal, Spain, Italy, Cyprus.

What's the common theme in these episodes? Conventional economics wisdom blames fiscal profligacy -- but in this whole list, that story fits only one country, Greece. Runaway bankers are a better story; they played a role in a number of these crises, from Chile to Sweden to Cyprus. But the best predictor of crisis is large inflows of foreign money: in all but a couple of the cases I just mentioned, the foundation for crisis was laid by a rush of foreign investors into a country, followed by a sudden rush out.

I am, of course, not the first person to notice the correlation between the freeing up of global capital and the proliferation of financial crises; Harvard's Dani Rodrik began banging this drum back in the 1990s. Until recently, however, it was possible to argue that the crisis problem was restricted to poorer nations, that wealthy economies were somehow immune to being whipsawed by love-'em-and-leave-'em global investors. That was a comforting thought -- but Europe's travails demonstrate that it was wishful thinking.

And it's not just Europe. In the last decade America, too, experienced a huge housing bubble fed by foreign money, followed by a nasty hangover after the bubble burst. The damage was mitigated by the fact that we borrowed in our own currency, but it's still our worst crisis since the 1930s.

-- Paul Krugman.

April 1, 2013

Tradelog Software for tax preparation

Tradelog Software does all the obvious things for traders' taxes; which is nice, because the IRS does not.

Broker 1099-B reports are often useless for tax reporting since the IRS has different rules for taxpayers than they do for brokerages. No, you did not read that wrong! Let me say that again: The IRS has different reporting rules for taxpayers than they do for brokerage 1099s. And in many cases (maybe as high as 90%) your brokerage 1099-B will not match with what you, the taxpayer, are required to report on Schedule D Form 8949.

Greene recommends it:

We frequently find errors in other programs and solutions on wash sales, tax treatment and more. Many of these programs or solutions are geared toward the needs of brokerage firms, and IRS rules for broker-issued securities 1099-Bs are materially different from what taxpayers need to report on their Form 8949/Schedule D. Brokers are permitted to report potential wash sales based on "identical positions," whereas taxpayers must report actual wash sales based on "substantially identical positions" (between stocks and stock options based on the same symbol). Many tax preparers get lazy and import broker-issued securities 1099-Bs into their tax preparation software which is a huge mistake, because it will either overstate or understate trading gains and losses

Also in tax: Coruscation: Tax for subway to the sea; Coruscation: Middle class by tax bracket in Westchester County, ....