Citibike angels program is pure arbitrage

Bike Angels forCitiBike NYC bike share.

Bike Angels forCitiBike NYC bike share.

Diane Garnick from TIAA; Chicago Booth

Date Written: February 27, 2017

Abstract

Mental Accounting is an important tool enabling us to make countless decisions each day. We code, categorize and evaluate our expenses using a system that we typically develop with our first paycheck. We routinely allocate some portion of our money to many buckets, and often over commit ourselves. 25% to housing, 25% to food, 25% to loans, and of course, another 50% to entertainment. We don't necessarily make the best decisions, but if we make a mistake we have time on our side.

Mental Accounting in Retirement involves a key change in mindset. Time is no longer on our side and (hopefully) our level of wealth is higher. Rather than allocate some funds to many buckets we propose fully funding one bucket before moving on to the next. This framework offers transparency into the age old question of how much guaranteed lifetime income each household needs while simultaneously offering savers insight into which goals they are on track to meet.

Keywords: Behavioral Finance, Mental Accounting, Mental Accounting in Retirement, Emotional Accounting, Lifetime Income, Psychological Biases, Behavioural Finance

JEL Classification: A10, D03, D10, D91

The for-profit Art Institutes programs that failed the federal test trained students in fields including commercial photography, video production, radio broadcasting, culinary arts, interior decorating and video game design. Other programs that crop up frequently on the failing list include cosmetology and barbering, acupuncture and massage therapy, criminal justice studies and low-level jobs in health care fields.

What these programs have in common is a combination of marketing appeal to young people -- design video games for a living! -- and little or no outside pressure to ensure that the education is both of high quality and leads to jobs that pay enough to finance the cost of student loans. Sure, there are good programs in all of these fields, including some offered by for-profit schools. But it can be very hard for the average consumer to know the difference beforehand.

https://www.nytimes.com/2017/01/13/upshot/harvard-too-obamas-final-push-to-catch-predatory-colleges-is-revealing.html

You can argue that the problems caused by, say, Romanians using the National Health Service are exaggerated, and that the benefits of immigration greatly outweigh these costs. But that's a hard argument to make to a public frustrated by cuts in public services -- especially when the credibility of pro-E.U. experts is so low.

For that is the most frustrating thing about the E.U.: Nobody ever seems to acknowledge or learn from mistakes. If there's any soul-searching in Brussels or Berlin about Europe's terrible economic performance since 2008, it's very hard to find. And I feel some sympathy with Britons who just don't want to be tied to a system that offers so little accountability, even if leaving is economically costly.

An adviser (Dan Davies) for Frontline Analysts, a global research outsourcing firm, supports Remain.

"These kids have grown up with computers. They have been downloading movies and music since they were 10 years old, so it's not much of a leap to download credit card numbers."

-- said Lt. Timothy Fenfert, who leads the Police Department's Special Fraud Squad in Brooklyn.

LendingClub's problems this week, musings of Matt Levine:

LendingClub got in trouble for being too much like a FintTech -- a "financial technology" company -- and too little like a bank, focusing on algorithms and speed and coolness rather than the plodding legalistic work that is the actual business of finance.

LendingClub got in trouble for being too much like a bank and too little like a FinTech, with mission creep, conflicts of interest and "a complicated network of middlemen" instead of a pure technology-driven neutral platform.

Before the 1980s, Texas followed a long, populist tradition that tried to protect family farmers and other small-scale businesses and consumers. Under its 1876 constitution, for example, Texas enacted consumer protections against predatory mortgage lending, with provisions that ironically helped to hold down foreclosures in Texas during the Great Recession.

In 1889, Texas became the second state in the country to enact an antitrust law. Two years later, it further pioneered government regulation of big business by establishing the Texas Railroad Commission, which went on to protect wildcatters and other small-scale oil producers by regulating the oil industry in ways that kept outside Goliaths like Standard Oil at bay. But since the 1980s, "pro business" in Texas has more and more come to mean just pro Big Business.

Second Measure by Mike Babineau and Lillian Chou tracks business' sales for investors.

Second Measure takes billions of anonymized credit card transactions and analyzes them so investors can see where consumers are voting with their dollars before a company's quarterly earnings come out.

More in data.

Continue reading "Track business' sales to aid investors " »

Update: Inventory management 2.

When an automaker posts its sales figures at the end of the month, how many vehicles actually left the dealer lot?

Not all of them, according to a top BMW executive, who admitted that his company and others "punch" up sales numbers to boost their standing, according to Automotive News.

Punching cars is "not an ideal practice," but it's a reality in the industry, BMW of North America CEO Ludwig Willisch said on March 22.

Speaking at the National Automobile Dealers Association-J.D. Power Automotive Forum in New York, Willisch said there was "a lot of pressure" to boost sales numbers. The practice involves an automaker purchasing its own vehicles to serve as dealer loaners, then quickly re-selling them as pre-owned after having seen very little use.

The issue of punching arose from last year's close four-way battle for the top luxury automaker spot in the U.S., a battle BMW won -- on paper, at least.

Recording 346,023 U.S. sales in 2015, BMW placed first in the race and Lexus third, but when actual vehicle registrations were tallied, Lexus came out on top.

Numbers gathered by IHS Automotive/Polk showed a gap of 10,764 vehicles between BMW's sales and registration figures, the largest of the top three luxury automakers.

The program, called EB-5, allows wealthy foreign investors, for a price ranging from $500,000 to more than $1 million, to put themselves on a path to United States citizenship. The money must be used to finance a business in this country and eventually employ -- directly or indirectly -- at least 10 American workers in economically depressed areas.

But EB-5 has been the subject of increasing scrutiny since investigators uncovered numerous cases of fraud, discovered individuals with possible ties to Chinese and Iranian intelligence using fake documents and learned that international fugitives who have laundered money had infiltrated the program.

"It's no secret that the program has long been riddled with corruption and national security vulnerabilities," said Senator Charles E. Grassley, Republican of Iowa and a frequent critic of the program.

A number of Democrats echo his criticism, in large part because while most visa applicants must meet education or work requirements, the primary requirement for the EB-5 program is a "lawful source of investment income," one Department of Homeland Security memo said.

"I don't believe that America should be selling visas and eventually citizenship," said Senator Dianne Feinstein, Democrat of California, who wants to terminate a part of the program that allows foreign applicants to invest through regional development centers that pool investor money. "The right to immigrate should not be for sale."

Continue reading "Investor immigrants are lucrative criminals seeking refuge ?" »

Fintech insurgents are moving and growing quickly, they must overcome big challenges of their own before reshaping the industry. They are still relatively small and niche players in the sprawling retail banking business. They are not deposit-taking institutions, where consumer savings are insured by the government.

They also lack the legal and regulatory apparatus that traditional banks have built over many decades. Already, some of the new services are facing regulatory scrutiny. In November, Apple, Google, Amazon, PayPal and Intuit formed a Washington-based advocacy group, Financial Innovation Now, to promote policies to "foster greater innovation in financial services."

Goldman Sachs set up its first office in San Francisco in 1968. In the 1990s, Wall Street banks sought out "the Four Horsemen," a contingent of local boutique investment banks that had cornered the market on virtually all the tech start-ups. JPMorgan bought Hambrecht & Quist (Mr. Perkins has long said the only banker he ever liked was Bill Hambrecht of Hambrecht & Quist); Deutsche Bank bought Alex. Brown & Sons; the predecessor to Bank of America bought Robertson Stephens; and Montgomery Securities was bought by NationsBank (which later merged with Bank of America).

Andreessen Horowitz is a talent agency as much as a tech investor. Marc Andreessen, the web pioneer who was a founder of Netscape and other companies before trying his hand at venture capital, has made this point explicitly a in 2010 interview of Michael Ovitz, the onetime Hollywood superagent who started Creative Artists Agency.

The Renaissance Kids typically have their pick of investment banks, and what makes them so attractive to Wall Street -- aside from their credentials, which look good on a pitch book -- is that they're interesting. They're not carbon-copy Alex P. Keatons. They read books, can wax eloquent on nonfinancial matters, and are good at male small-talk (which female Renaissance Kids also excel at). Executives look them over and imagine them schmoozing clients, passing the airport test, and eventually taking over for them at the top of the firm.

Goldman Sachs is especially desirous of Renaissance Kids, because it's always fancied itself the thinking man's investment bank. ("I think you also have to be a complete person. You have to be interesting," Lloyd Blankfein told the bank's interns last year.) But because Goldman wants them, everyone else does, too.

The problem, for Goldman and the rest of Wall Street, is that banks aren't pulling nearly the number of Renaissance Kids they once did. These firms are having no problems drawing applicants out of college, but what I've heard from senior Wall Street hiring managers is that they're not the right kind of applicants. They're second-stringers, as far as the banks are concerned. The students these firms want to attract -- badly -- are increasingly going to Google or Facebook instead of Goldman and J.P. Morgan. (Or, almost worse, going to Goldman and J.P. Morgan, working for a year or two, and then quitting to go to Google or Facebook.)

How would I receive the proposed disclosure, if I obtained my prepaid card at a retail store, rather than at a bank branch?

Pew is proposing a "fold out" version of its disclosure form that would be available in stores on the same hooks that display the prepaid cards. Right now, disclosures are typically contained inside the package containing the card, so consumers can't see them ahead of time, and they are often difficult to read, Susan K. Weinstock, director of Pew's safe checking research project said.

If there was a competition entitled "Correct the analyst's spreadsheet", that could be sort of cool, right?

The Stratton brokers could have just placed orders in these customers' accounts without their permission, but they rarely did. Unauthorized orders were more likely to trigger complaints to regulators, and the move would have violated some unofficial boiler-room code of honor. These guys took pride in their ability to talk suckers into parting with their life savings.

-- Ronald Rubin

Why have no top Wall Street executives have been charged criminally for the risky acts that triggered the crisis. The government also prefers to settle with big companies rather indict them, fearing that criminal charges could unnerve the broader economy.

The government investigations into JPMorgan, which focus on securities the bank sold from 2005 to 2007, raised questions about whether JPMorgan had failed to fully warn investors about the risks of the deals.

One of the largest pieces of the $13 billion deal could come from a settlement with the Federal Housing Finance Agency. The agency sued JPMorgan over loans it had sold to Fannie Mae and Freddie Mac, the government-controlled mortgage finance companies.

The settlement would also resolve a case related to Bear Stearns, the people briefed on the matter said, a lawsuit that has pitted the New York attorney general against JPMorgan.

Eric T. Schneiderman, the New York attorney general, sued JPMorgan last October, saying Bear Stearns and its lending unit, EMC Mortgage, had duped investors who bought mortgage securities assembled by the companies from 2005 through 2007. Through a deal backstopped by the government, JPMorgan bought Bear Stearns in 2008.

Mr. Dimon has called the lawsuit unfair, arguing that JPMorgan should not be penalized for buying Bear Stearns.

Yet JPMorgan's board, faced with regulatory problems, one more vexing than the next, is eager to strike a conciliatory stance. Toward that end, the bank's board approved the payment of about $1 billion in fines to government authorities so it could resolve investigations into the trading loss in London and an inquiry into the bank's credit card products.

But the accountants' job is to record, not to evaluate. The evaluation job falls to investors and managers. Accounting numbers, of course, are the language of business and as such are of enormous help to anyone evaluating the worth of a business and tracking its progress. Charlie and I would be lost without these numbers: they invariably are the starting point for us in evaluating our own businesses and those of others. Managers and owners need to remember, however, that accounting is but an aid to business thinking, never a substitute for it.

-- Warren Buffett

Uncertainty and the Oil Fields

The reason for the review is that an Australian scholar has recently published a paper offering "A Bayesian Understanding of Information Uncertainty and the Cost of Capital." The gist of it is that traders face information uncertainty, that is, the risk of a misleading signal about the value of an asset.

"The Bayesian position," says D.J. Johnstone of the University of Sydney Business School, "is that even a highly informative signal ... can bring an increase in uncertainty, and hence an increase in the cost of capital." This is at least somewhat counter-intuitive. Surely the highly informative signals (also known as "greater transparency") will lessen uncertainty and risk, thus reducing the cost of capital.

Ah, Johnstone says, perhaps not. Consider a world in which there are two possible geological formations involved in the search for oil: A and B. There may be oil under either plot. Geologists tell us that plot A belongs to a type of geological formation with a 0.5 frequency of oil. B-type plots, on the other hand, have a 0.95 frequency of oil. It isn't always obvious which is which, and oil companies like to figure out which is which before making the final decisive test to determine whether there is oil there.

Suppose also that the prior probability of oil under a random site, before we even know if the site is A or B, is 0.635.

Now, on Day 1, an oil company owns a piece of land that has not yet been tested for oil, or even tested to determine whether it is A or B. The market will presumably assess the value of this land accordingly. Prospective buyers will consider it as having a 0.635 likelihood of bearing oil.

On Day 2, the land is tested and found to be of Type A.

Thereafter, the market will lower the value of that land, because its likelihood of bearing oil has fallen to 0.5. There is greater uncertainty post-test than there was pre-test.

Continue reading "Understanding of Information Uncertainty and the Cost of Capital" »

In 2011, Jamie Dimon, chief executive of JPMorgan Chase, said that the proposed rules to overhaul derivatives, a commonly used financial instrument, "would damage America." He also said that the Basel rules were "anti-American." Comment letters filed by lobbyists with regulators used sophisticated-looking models to show how rules could hold back the economy.

"As far as the banks are concerned, there is never a good time to raise capital or increase regulation," Ms. Bair said. "When times are bad, they say it could hurt things, and when times are good, they say they don't need it."

Some analysts, however, caution against reading too much into the banks' strong profits.

Though banks have been preparing for new rules for months, many of them have not been fully executed, which means the true costs of the measures will not be known until later.

Michael Poulos of Oliver Wyman, a consultancy, says that "before the crisis, almost every bank account made money. Big accounts made money on the spread, and small accounts made money on incident fees. You made money on all the accounts with interchange fees. All of that is either severely curtailed or completely gone." Oliver Wyman reckons that US banks now lose money on 37% of consumer accounts.

For those concerned that their low net worth bars them from the banking system, there are two reasons for hope. The first is that lenders and credit bureaus are starting to use a broader range of data to determine the creditworthiness of prospective borrowers. Many of the unbanked have no credit histories. But data from rent, mobile-phone and utility bills give lenders a way to find lower-risk borrowers.

The second reason for optimism is an increasingly competitive market in pre-paid cards. Once simply reloadable proxies for cash, many of these cards now offer much the same features as bank accounts.

Taxes: Oh yeah, and I haven't assumed any taxes on the above calculations. In recent years, unrealized gains seems to be offset by losses (note the deep discount to book value of CNA). So it would be a wash. Plus, these folks tend not to pay taxes. I think any monetization will come through spinoffs, exchanges and other tax efficient means. Part of the discount in L stock might be due to people applying 20% discounts to the value of publicly listed holdings for tax and liquidity. It may be the correct way to look at things, but I'm not convinced enough to put it in my valuations.

Conclusion: Anyway, this L is a really boring stock

Brooklyninvestor's Loews adjusted book value update.

Part 2 is up.

The potential downgrades would cost those institutions billions of dollars in higher interest payments, steeper collateral costs and missed revenue opportunities.

What's making executives at Morgan Stanley and the scores of rivals waiting for Moody's decisions even more frustrated is they are fighting against an army of credit-rating analysts who are nowhere near as well-known and are paid a fraction of what bankers get. Even finding someone to blame can prove elusive, as Moody's ratings actions are decided by a voting committee of about a dozen analysts whose identities are never disclosed.

Moody's actions are faceless by design. The aim is to shroud at-times contentious decisions in an aura of mechanic precision, and to protect its analysts from the personalized attacks they may otherwise endure from finance ministers, bank executives and other debt issuers unhappy with their decisions.

While most people welcome leverage limits as the just consequence of Wall Street's greed, and conclude that we will be safer if these businesses are run more prosaically, there is a real danger that we have focused on the wrong problem, and will condemn our once enviable capital markets to a period of bland ineffectiveness. While lower leverage would certainly provide more of a margin against the inevitable future errors of Wall Street executives, hard limits on risk-taking might also lead to stifled innovation and slow economic growth. Would Michael Milken, at Drexel Burnham, still have created the junk-bond market--or Lewis Ranieri, at Salomon Brothers, the securitization market--if the Dodd-Frank law or the Volcker Rule had been around to curb their firms' ability to take risk?

The spread and evolution of the idea that the financial crisis was caused by a giant increase in leverage, enabled by the SEC, bears a passing resemblance to the old-fashioned, elementary-school game of telephone. While the change to the SEC's so-called net-capital rule in 2004 was plenty esoteric, in the main, it did not allow big securities firms to take on more leverage. The SEC did two things in 2004: First, it assumed the added responsibility of regulating Wall Street's larger holding companies--as opposed to just the broker-dealer subsidiaries within them. That's where more and more funky and risky assets, such as derivatives and mortgages, had been housed over the years. Second, the SEC required the holding companies to report their capital adequacy in a way that was consistent with international standards, and to discount their assets for market, credit, and operational risks. Clearly, the SEC did a poor job of monitoring Wall Street once it obtained this increased regulatory authority. But the rule change increased rather than decreased the SEC's oversight of the financial sector, and did not suddenly permit a dramatic increase in leverage.

Yet that's not how the rule change got interpreted. In the aftermath of the collapse of Bear Stearns, in March 2008, people were eager to know how a company that had thrived for 85 years, and that had $18 billion in cash on its balance sheet, could evaporate in a week's time. Enter Lee Pickard, a former director of the SEC's trading-and-markets division and one of the architects of the net-capital rule in 1975. In an August 2008 essay in American Banker, Pickard lambasted the 2004 change, which he believed had allowed Bear Stearns to incur "high debt leverage" without "substantially increasing [its] capital base." He argued that the original net-capital rule required securities firms to discount, or "haircut," the value of their assets depending on the assets' perceived risk, and that it limited the amount of debt they could incur "to about 12 times [their] net capital." After the SEC's 2004 rule change, he wrote, the large securities firms were permitted to avoid the haircuts and the limitations on indebtedness. According to Pickard, "The losses incurred by Bear Stearns and other large broker-dealers" were caused "by inadequate net capital and the lack of constraints on the incurring of debt."

Morgan Stanley deserves credit since it did not fire Barton Biggs, Byron Wien, or Stephen Roach during that period when most Wall Street firms replaced nourishment with treacle.

Two events come to mind.

In the summer of 1999, Barton Biggs debated James K. Glassman. This was the high summer - or, at least, the final summer - of the Internet bubble. It was obviously ridiculous but there was still time to get rich quick. To quote myself: "During the first four months of 1999, the average first-day percentage gains on IPOs were 271% (in January), 145% (February), 146% (March) and (119%) in April. More to the point is the lack of any operating record on the part of these enterprises. They were often no more than lavish compensation schemes for the promoters. Many of the companies had never earned a cent; quite often, they had never sold a thing; and not infrequently, they had neither a product to sell nor intended to develop a business.

"The book that captured the national idiom was Dow 36,000, by James K. Glassman and Kevin Hassett. They posted a preview on the editorial page of the Wall Street Journal on March 17, 1999: "Our calculations show that with earnings growing in the long-term at the same rate as the gross domestic product, and Treasury bonds below 6%, a perfectly reasonable level for the Dow would be 36,000 - tomorrow, not 10 or 20 years from now."

The debate between Biggs and Glassman is a classic example of people believing what they want to believe while ignoring the proverbial elephant in the room. Of course, in 2012, the obvious catastrophic consequences of central banking's destruction of the world's currencies as well as stock, bond, and commodities markets are not up for discussion.

-- Frederick Sheehan

Continue reading "Barton Biggs vs James K. Glassman and Kevin Hassett" »

Though smartphone payments have a long way to go before they replace wallets altogether, Starbucks's adoption of Square will catapult the start-up's technology onto street corners nationwide, and is the clearest sign yet that mobile payments could become mainstream.

"Anyone who's going to break the mobile payments barrier in the U.S. has to overcome the resistance to try anything new when everything we have works really, really well, even cash, which is very convenient," said Bill Maurer, director of the Institute for Money, Technology and Financial Inclusion at the University of California, Irvine.

Signing up for Square involves supplying your bank routing and account numbers, so Square can deposit your money. Only the first $1,000 of each week's charges lands in your bank account immediately. Anything over that is reviewed by the company's auditors; it can take as long as 30 days before you see the rest of the money. That could be a downside if you sell a lot of used cars.

Then again, that's just for first-timers. The more you use the service without incident, the higher the company will raise that $1,000 threshold. In fact, if you're willing to share more details about your business with Square upfront, they'll raise that threshold from the start.

When everyone agrees, prices get stupid. Studies have shown that crowd estimates can be surprisingly accurate on average -- but only when there is sufficient diversity of opinion. Market valuations are the same way: When you have a diversity of opinion, reasonable estimates prevail as outliers cancel each other out. But when there is a critical mass of one-sided opinion -- when an overwhelming majority shares the same general view -- you get serious mispricings.

For Javaid Tariq, a taxi driver in New York City who sends money monthly to his family in Pakistan, the exchange rate is particularly infuriating because of how much money he loses. When he sent $300 to his family in April, he received 89.2 rupees for every dollar, less than the 91.2 exchange rate that he checks each morning, he said. For his family, that means 599 fewer rupees, or more than a week's salary in Lahore.

Immigrant advocates argue that many people do not have time to shop for better rates.

"These are people working who are often working minimum wage jobs with very little savvy or time about where to price-shop," said Francis Calpotura, the founder and director of the Transnational Institute for Grassroots Research and Action in Oakland, Calif.

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/78b9df70-a978-11e1-9772-00144feabdc0.html#ixzz1wg4ig5p1

We need to adopt a corporate performance statement that is transparent and relevant for assessing value. This should include two separate sections: the cash flows the company realised during the reporting period and estimates of the company's future cash flow commitments. The statement begins with revenue and deducts cash outlays for operating expenses and capital investments to arrive at free cash flow. This is the cash available to pay interest and dividends and gives investors a baseline from which they can assess the company's prospects. Clearly stating the individual items that determine free cash flow is the best way to serve investors.

The second section presents estimates of the cash flows that the company anticipates it will need to satisfy future financial commitments, such as pension liabilities. Reporting a single estimate to capture an uncertain amount leaves investors in the dark. This corporate performance statement presents a most likely, an optimistic and a pessimistic estimate for each account. Management's discussion of the factors driving the estimates and the likelihood of each enables investors to form their own expectations in an informed fashion.

Continue reading "Beyond point estimates, financial statements edition" »

The SAS financial services modeling group in San Diego, exploring ways they can take advantage of high-performance analytics and big data techniques to deliver more models, more quickly, and to more customers. This wasn't completely an academic exercise--the team in San Diego has added several new customers recently and have been looking for ways to boost productivity, so this is the perfect setup for our high-performance story. Perhaps you've seen Jim Davis' blog where he ponders what you can do with all the extra time savings that high-performance analytics offers ... provide service to more customers is one good idea!

The biggest threat to incumbents, however, comes from outside the traditional banking sector, where hungry innovators are trying to cut the cost of investment advice and wealth management drastically. The most fertile ground for many of these new firms is in California, where a generation of technology entrepreneurs that made its money online is preparing to invest it online too. The region is already awash with traditional wealth managers. UBS, Goldman Sachs, JPMorgan and others are expanding in San Francisco and around Silicon Valley. They have recently been joined by online rivals such as Wealthfront, MarketRiders and Personal Capital, all of which use technology to help clients build customised asset portfolios at a small fraction of what traditional wealth managers would charge.

The biggest threat to incumbents comes from outside the banking sector, where hungry innovators are trying to cut the cost of wealth management.

Wealthfront, which is aiming its offering squarely at Silicon Valley's new rich, will manage money for a fee of 0.25% a year, using sophisticated algorithms that measure risk tolerance and build a diversified portfolio. Another new entrant is Personal Capital, started by Bill Harris, a former chief executive of PayPal and Intuit. It tries to straddle the world between cheap online wealth management and the old world of private banking. Customers can sign up online but the firm provides expert portfolio and tax-management advice and assigns wealth managers to individual customers. In Britain a firm called DCisions has crunched the data on millions of portfolios to obtain risk-adjusted returns as benchmarks for new investors. The data show up clearly how wealth managers' fees have affected the value of the portfolios and what difference the managers' advice has made.

Tom Blaisdell, a partner at DCM, a venture fund, manages his savings through MarketRiders. For a flat fee of $14.95 a month the firm assesses his tolerance for investment risk and helps him construct a portfolio of investments using exchange-traded funds that he can buy through any discount broker. The firm monitors his asset allocation as markets move and sends him quarterly instructions on what to buy or sell to rebalance his portfolio. "I've got a personal rant on this but 90% of what people call 'investing' in this country is what I call 'gambling'," says Mr Blaisdell. "It is a big area for innovation."

"STRATEGICALLY, I THINK in terms of millionaires and billionaires," says Jürg Zeltner, the head of wealth management at UBS, a Swiss bank. It is a claim that many big banks would like to make about their clients. Few can. With a squeeze on revenues from banking services for more down-at-heel folk, many of the world's biggest banks, as well as some smaller ones, hope to plump up their profit margins by serving the very wealthy. Yet margins in private banking and wealth management are also being squeezed, and new competitors from outside banking stand a good chance of breaking into this market.

Self-evidently, the big attraction for banks is that rich people have more money to invest and spend on advice than poorer ones. Definitions of rich customers vary from bank to bank and region to region, but there is a rough pecking order. Customers with financial assets above $1m (not counting their homes or businesses) are generally classified as high-net-worth individuals, and those with assets of $10m-30m as ultra-high-net-worth. The Boston Consulting Group puts the total investible assets of the world's wealthy at around $122 trillion last year, almost enough to buy all the shares traded on the New York Stock Exchange ten times over. Capgemini and Merrill Lynch come up with a more modest estimate of about $43 trillion. Whichever number is right, the market is certainly big enough to be interesting; and everyone agrees that it is growing quickly. The rich world is still home to most of the world's money: about a third is in America and another third in Europe. Yet the fastest growth is in Asia, where the assets of the rich increased by almost a fifth in 2010

Spitzer forced an industry-wide settlement in which the involvement of research analysts in IPOs was pared back and the "Chinese Wall" between research and banking was strengthened.

This industry reform had several consequences, some of which were positive and some of which were negative.

On the positive side, the reforms removed some stress for analysts. Once analysts were no longer evaluated in part on banking business, they focused more on serving institutional investor clients and researching already public companies. And that's unequivocally a good thing.

On the negative side, it became harder for companies to go public...because it turned out that having analysts involved in the screening, positioning, and marketing of deals and then providing follow-on research coverage of small companies made the whole IPO process work better. So that, arguably, was a bad thing.

Read more: Henry Blodget / businessinsider

Continue reading "Facebook IPO, why it's different from the dotcom ere $FB -- Blodget" »

Zuckerberg's torture-by-attorney didn't start in the past twenty-four hours, when law firms in New York and California initiated the first of what is sure to be a slew of lawsuits related to last week's controversial I.P.O. Ever since February, when Facebook filed its initial investment prospectus, the youthful C.E.O. has had to check with his own lawyers before saying virtually anything publicly--a requirement imposed as part of the S.E.C.'s pre-I.P.O. "quiet period," which applies to any company preparing to issue stock.

At that time, Wall Street research was under a microscope. Eliot Spitzer, then the New York attorney general, had exposed how analysts routinely slanted research to win lucrative investment banking business. In 2003, Lehman was among 10 firms that reached a $1.4 billion settlement. They all promised to wall off research operations from other parts of their business.

But Ted Parmigiani, says he was asked to break those new rules. Lehman bosses, he contends, told him to write research that would support investment banking business -- a violation of the Spitzer settlement. He says he was warned not to make negative comments about companies, even when he thought they were merited, lest he antagonize corporate executives. In 2003, he says, he was chastised for downgrading a company that was a corporate finance client of Lehman's.

Most alarming, Mr. Parmigiani says, was that Lehman had created a system that gave its stock trading desks access to its analysts' research recommendations before those recommendations were made public. The Product Management Group, as this business unit was known, scheduled analysts' calls on the firm-wide squawk box system and was part of the research department.

Mr. Parmigiani says the Product Management Group often delayed the announcements of recommendation changes for no apparent reason. He says he began to suspect that the delays were meant to allow Lehman's traders to put on positions ahead of the news and to give the firm's top sales representatives time to alert favored clients.

On March 30, 2005, Mr. Parmigiani had been scheduled to meet with a series of hedge fund clients, including Moore Capital, to discuss his research. At the last minute, Jared Demark, a vice president in Lehman's institutional equity sales who covered the hedge funds and had planned to accompany him, bowed out. In an e-mail to Mr. Parmigiani, Mr. Demark wrote: "Go to the Moore meeting without me, we have big ratings change looming ... "

While Mr. Parmigiani did not learn precisely what Mr. Demark meant by that e-mail, it fueled Mr. Parmigiani's concern that Lehman was alerting hedge funds to analysts' pending changes.

Lending Support to Kyes : Immigrants' Credit Associations Need to Be Encouraged--for Everyone's Financial Health

Voices

October 24, 1993. Ivan Light, a professor of sociology at UCLA, is the co-author of "Immigrant Entrepreneurs: Koreans in Los Angeles, 1965-1982." (Los Angeles: University of California, 1988).

When Jung-Hie Park sought to collect $50,000 owed to his kye , a popular financial institution in the Korean community, he turned to California courts for adjudication. Without examining the merits of his claims, Superior Court Judge Edward M. Ross ruled in September that kyes were an "illegal lottery" whose debts could not be collected in an American court.

Although Ross' decision may be appealed, it highlights the difficulty that American law encounters when attempting to digest foreign saving and credit institutions like the kye . In the language of anthropology, the Korean kye , the Mexican tanda , the Chinese hui , and the Vietnamese ho are examples of the rotating savings and credit association, a popular financial institution of the Third World

Continue reading "Kye ( Gye ), social credit of Korean America" »

To the auditing industry, the fact that investors tend to blame auditors when frauds go undetected reflects unrealistic expectations, not bad work by the auditors. The rules say auditors are supposed to have a "healthy degree of skepticism," but not to detect all frauds.

"There is a significant expectations gap between what various stakeholders believe auditors do or should do in detecting fraud, and what audit networks are actually capable of doing, at the prices that companies or investors are willing to pay for audits," stated a position paper issued in 2006 by the chief executives of the six largest audit networks.

Note that last part. They suggested that if investors were really worried about fraud, they should consider paying more for a "forensic audit" that would have a better -- but not guaranteed -- chance of spotting fraud. Don't like our work? Pay us more.

Ernst's audit opinion does not say, which is no surprise. Virtually every audit opinion in the world says almost the same thing, with no details about the company being audited. Auditors are paid millions of dollars to produce a report that no one thinks is worth reading.

On June 21, the Public Company Accounting Oversight Board, which regulates auditors in the United States, plans to ask for public comments on whether to require auditors to do more and say more.

One idea the board is expected to consider is requiring auditors to disclose more about what they did, and did not, do. Ideally, auditors would point to things that they could not audit. There are a lot of them now, and sometimes they are crucial.

Andy Haldane, the-regulator-who-explained.

Also: Andrew Haldane asks "Is the world becoming more short-sighted?" (Bank of England)

Under one equilibrium, patience wins the day. When long-term investors start in the ascendency, prices tend to correct towards fundamentals. The performance of untested investors pursuing momentum strategies falters, while those pursuing longterm strategies flourish. The fraction of long-term investors rises. The self-correcting tendencies of market prices are thus reinforced, further supporting long-term investors. The patience gene thrives, the impatience gene dies. Natural selection results in a self-improving cycle, as with dieting, happiness and exercise.

But there is a second equilibrium where this cycle operates in reverse gear. With a large fraction of momentum traders, prices deviate persistently from fundamentals. Among untested investors, momentum strategies now flourish while long-term fundamentalists fail. The speculative balance of investors rises, increasing the degree of misalignment in prices. The patience gene falls into terminal decline. Natural selection results in a self-destructive cycle, as with drug, alcohol and food addiction.

The recent financial crisis has generated many distinct perspectives from various quarters. In this article, I review a diverse set of 21 books on the crisis, 11 written by academics, and 10 written by journalists and one former Treasury Secretary. No single narrative emerges from this broad and often contradictory collection of interpretations, but the sheer variety of conclusions is informative, and underscores the desperate need for the economics profession to establish a single set of facts from which more accurate inferences and narratives can be constructed.

-- Andrew Lo

If migrants spent heavily, lenders encouraged them. Traditionally, credit card use was low (in part because of Islamic strictures against charging interest), but banks spotted a new market and moved aggressively.

With foreign banks like HSBC and Citigroup fighting locals for market share, the number of cards leapt to four million in 2008, a fivefold increase in five years, according to the Lafferty Group, a London research firm. But the country lacks a reliable credit bureau, so lenders could not tell how many cards or how much debt the borrowers carried.

"Banks were falling over themselves to lend, and they didn't have proper credit checks," said Andrew Neeson, a Lafferty analyst.

Courted with gifts and teaser rates, few borrowers understood the costs. The average interest rate in the Emirates last year, at 36 percent, was more than twice the global average, and banks routinely add another 10 percent for disability and death insurance. With penalties, some workers borrowed at rates of 50 percent or more.

Anyone can be tempted by easy credit, but migrants raised in poverty can find the glittering malls here especially intoxicating.

"The first time I used my card, I felt amazed," Ms. Naces said. "It's a feeling of excitement, power -- greatness even."

Rex Arcenio, a Filipino optometrist, accepted a gold card because it came with a Montblanc pen and a limousine ride to the airport for his annual leave.

"It was like a status symbol," he said.

He ran up $50,000 in debt -- for his children's education, his brother's cancer treatment and a house in Manila -- and was briefly jailed.

Technically, debtors go to jail for bouncing the blank "security checks" they must sign when accepting a card. If borrowers fail to pay, banks can deposit the checks for the sum owed, and bouncing a check is a crime.

Whether foreign or Emirati, borrowers must repay the debt after leaving jail, though banks often accept reduced terms.

If the greed of Boesky or Weill is unsurprising, the lack of greed evinced by some of Madrick's characters is striking. Paul Volcker, the Fed chairman whom Madrick eccentrically berates for his determined fight against inflation, was known to be frugal; John Reed, Citigroup's boss during the 1990s, was by Madrick's own account "thoughtful and unflashy." Reagan himself was more enthusiastic about self-reliance and hard work than about material advancement, remarking that "free enterprise is not a hunting license." Early in his career, Walter Wriston, Reed's predecessor at Citi and perhaps the character whom Madrick conjures most successfully, was offered a salary of $1 million to move to Monaco and work for Aristotle Onassis. He chose to remain in a middle-income housing project in Stuyvesant Village.

Age of Greed: The Triumph of Finance and the Decline of America, 1970 to the Present

Sebastian Mallaby -- the Paul A. Volcker senior fellow at the Council on Foreign Relations, is the author of "More Money Than God: Hedge Funds and the Making of a New Elite."

BOOKS

Why We Deregulated the Banks

By SEBASTIAN MALLABY

Published: July 29, 2011

Jeff Madrick traces the regulatory and cultural changes that led to America's current financial trouble.

"Look, if you can't compete in the major leagues for over a decade, it's time to go back to the minors," said the always outspoken Mike Mayo, an analyst with CLSA. His chronicle of ruffling bank management feathers, "Exile on Wall Street" (Wiley), will be published in the fall.

JPMorgan Chase is as well managed as any gargantuan bank can be. But if you look at its businesses, it's hard to see any area where it is clearly the best, something even its own executives concede. Not in credit cards, where the premier name is American Express. Not in money management, where you might offer up T. Rowe Price. Investment banking -- Goldman Sachs (the last quarter notwithstanding). Back-office transactions, State Street.

Yet even JPMorgan is merely trading at book value. Put another way, the market regards the value that JPMorgan provides as a financial services conglomerate as zilch. How well do all of JPMorgan's divisions work together? In presentations to investors, JPMorgan executives show how much revenue they gain from existing clients. But these measures are hardly unbiased. Executives have an incentive to defend their empires. Who is to say that a certain division of JPMorgan wouldn't have won that business anyway? And nobody measures how much a bank loses through conflicts of interest.

Making a nuanced argument, John Hempton, a blogger, investor and former regulator in Australia, says that it's better for shareholders -- and societies -- to have large banks with lots of market power. That makes them more profitable and leads them to take less risk, making them safer and more enticing for investors.

South American countries -- including Chile and Brazil, two of the region's healthiest economies -- are going through growing pains as the use of credit grows. The credit-fueled spending has driven extensive economic growth. But it has also opened the door to abuses, as credit issuers have used predatory techniques to lure customers, particularly young and less affluent ones, in countries where regulation is scant, annual interest charges can top 220 percent and consumers cannot seek bankruptcy protection, economists and consumer defense groups say.

"They are learning every trick that was learned in the United States to make credit cards the most valuable part of the banking business," said Lewis Mandell, a professor emeritus at the State University of New York at Buffalo, who wrote a book on the history of the credit card industry. "And unfortunately, the problems this caused in the United States are likely to repeat themselves in Latin America."

though the for-profit system serves only a little more than a tenth of those in postsecondary education, it accounts for nearly half of student loan defaults. The losses are generally of little concern to the companies themselves, because most of the tuition is paid by federal loans backed by the taxpayer. The defaulting students often end up with their lives in financial ruin.

Bankruptcy makes it possible to escape credit card and gambling debt but nearly impossible to escape student loan debt. As a result, students who default on school loans may never be able to have that weight lifted and can end up with creditors garnishing their wages.

The Obama administration has tried to address these problems with new rules to make programs with especially high levels of student debt and very low repayment rates ineligible for federal student aid. But these rules are insufficient.

Continue reading "For-profit colleges that leave students with crushing debt." »

n 2003, the Senate Permanent Subcommittee on Investigations looked into such transactions and found that in some cases, they were an elaborate way of using a charity's tax-exempt status to erase tax liabilities for the other shareholders of the company involved.

A charity involved in such a tax strategy would receive income from the company in proportion to the size of its holdings of nonvoting stock. But while that income was taxable, it was not distributed to the charity and stayed at the company to be reinvested.

The charity did not owe taxes on the income, anyway, because it was tax-exempt.

Later, the charity would sell the nonvoting shares back to the company at fair market value, and the company would distribute the income, tax-free, that had been associated with those shares among its other shareholders.

In other, similar cases, charities that received nonvoting stakes in privately held companies through gifts of stock used large losses they had incurred on unrelated businesses to offset taxes for other shareholders. Mr. Dryburgh wrote a paper on that type of tax shelter.

In 2004, the I.R.S. listed as "restricted" such transactions and denied deductions associated with them.

How a CPA would identify financial strength:

Cash to Equity

Underbillings

Quick Ratio

Current Ratio

Overbillings to underbillings

Long Term Debt to Equity

Return on Total Assets

Gross Profit

Contract Revenue to Working Capital

Revenues too Net Worth

Months in Backlog

The conventional wisdom has it that the final report of the Financial Crisis Inquiry Commission was a low-budget flop, hopelessly riven by internal political disputes and dissension among the commission's 10 members. As usual, the conventional wisdom is completely wrong. Actually, the report -- and the online archive of testimony, interviews and documents that are now available -- is a treasure trove of invaluable information about the causes and consequences of the Great Recession.

What one might call intellectual capture. While I would strongly argue that the FSA in my day did not favor firms unduly, it is perhaps true that we--and in this we were exactly like our American counterparts--were inclined to believe that markets were generally efficient. If willing buyers and willing sellers were trading claims happily, then, as long as they were "professional" investors, there was no legitimate reason to interfere in their markets. These people were "consenting adults in private," and the state should avert its gaze.

We now know that some of these market emperors had no clothes--and that their activities were far from benign: They could result in severe financial instability and generate serious losses for taxpayers, not to mention precipitate a global recession. That has been a grave lesson for regulators and central banks.

-- Howard Davies, former chairman of Britain's Financial Services Authority and a former deputy governor of the Bank of England, is director of the London School of Economics. His latest book is Banking on the Future: The Fall and Rise of Central Banking.

Abstract: The rapid growth of the market-based financial system since the mid-1980s changed the nature of financial intermediation in the United States profoundly. Within the market-based financial system, "shadow banks" are particularly important institutions. Shadow banks are financial intermediaries that conduct maturity, credit, and liquidity transformation without access to central bank liquidity or public sector credit guarantees. Examples of shadow banks include finance companies, asset-backed commercial paper (ABCP) conduits, limited-purpose finance companies, structured investment vehicles, credit hedge funds, money market mutual funds, securities lenders, and government-sponsored enterprises.

Shadow banks are interconnected along a vertically integrated, long intermediation chain, which intermediates credit through a wide range of securitization and secured funding techniques such as ABCP, asset-backed securities, collateralized debt obligations, and repo. This intermediation chain binds shadow banks into a network, which is the shadow banking system. The shadow banking system rivals the traditional banking system in the intermediation of credit to households and businesses. Over the past decade, the shadow banking system provided sources of inexpensive funding for credit by converting opaque, risky, long-term assets into money-like and seemingly riskless short-term liabilities. Maturity and credit transformation in the shadow banking system thus contributed significantly to asset bubbles in residential and commercial real estate markets prior to the financial crisis.

We document that the shadow banking system became severely strained during the financial crisis because, like traditional banks, shadow banks conduct credit, maturity, and liquidity transformation, but unlike traditional financial intermediaries, they lack access to public sources of liquidity, such as the Federal Reserve's discount window, or public sources of insurance, such as federal deposit insurance. The liquidity facilities of the Federal Reserve and other government agencies' guarantee schemes were a direct response to the liquidity and capital shortfalls of shadow banks and, effectively, provided either a backstop to credit intermediation by the shadow banking system or to traditional banks for the exposure to shadow banks. Our paper documents the institutional features of shadow banks, discusses their economic roles, and analyzes their relation to the traditional banking system.

First there's the cost: For-profit colleges are often much more expensive than comparable public ones. According to a report by the Government Accountability Office, one for-profit institution charged $14,000 for a certificate in computer-aided drafting that a local community college offered for just $520.

Then there's the issue of how the cost is covered: for-profit colleges take a disproportionate share of federal education loans. Although only 12 percent of post-secondary students go to for-profit colleges, they account for 23 percent of federal loans. And students at for-profit schools default on their loans twice as often as their public school counterparts, leaving taxpayers with the bill.

This is partly due to the open enrollment policies at for-profit colleges. It's disturbingly easy to get accepted, receive thousands of dollars in loans and then flunk out with crippling debt and no degree to show for it. I'm about to fail 4 out of 11 students in one of my classes because they simply stopped showing up. Some students will fail anywhere, but at this rate it's clear that many of them should never have been sold on the program in the first place.

I've also been on the other end of these sales tactics. I once looked into taking a class at a for-profit college. The admissions counselor was quite skillful at avoiding my questions about costs, and pressed me to enroll in a full degree program, despite my repeated refusals.

Problems with the for-profit business model don't end with recruitment; they extend to the classroom. While my nonprofit orientation covered how to create a syllabus and relate to students, the for-profit session addressed the importance of creating paper trails on attendance, should a student need to be flunked, and a video on how to avoid getting sued.

Here's the part that's really going to make me unpopular at my next faculty meeting. Many of my colleagues are excellent teachers, but their qualifications aren't much of a priority for the college. While teachers at a state or private university are typically expected to hold M.F.A.'s or Ph.D.'s, for-profit teachers need only to have taken a few hours of graduate course work.

Teachers at for-profits are paid less, and work more. Full-time instructors teach up to four times as many classes as their state school counterparts. And although nobody teaches only for the money -- I gross just over $30,000 a year, summers on, no benefits -- I earn 50 percent to 65 percent more at nonprofits. I try to treat both jobs with the same seriousness, but I'd be lying if I said this was always the case.

The business model of for-profit schools may pay off for shareholders -- just ask Goldman Sachs, which controls a third of the parent company of my for-profit employer, the Art Institute of Colorado -- but it clearly isn't as effective at educating students.

-- Jeremy Dehn teacher of film and video production at the University of Denver, the Art Institute of Colorado and the University of Colorado at Denver.

Under the current rules, schools with default rates of 25 percent or more for three consecutive years, or a default rate higher than 40 percent in a single year, lose their

eligibility for the federal student aid that provides most of the revenues for for-profit colleges.

Frederick Peters, the owner of Warburg Realty Partners, had run his business well in the 30 years he had owned Warburg Realty. Now through no fault of his own he found himself in a financial crisis that threatened the future of his firm. This was the definition of a clutch situation. Over the next few months, he responded well because his actions were guided by the five traits of people who are great under pressure:

He also avoided the three traps that cause most people to choke:

Alec Haverstick II, a co-founder of Boxwood Strategic Advisers, provided a tool that could take the passion out of financial decision-making. His rule was that when you have less than 12 months of cash left to cover your debt payments, you need to start selling assets. His prescription applied to anyone because the advice was not based on having a lot of money so much as being smart with the money you have left.

In "Fault Lines: How Hidden Fractures Still Threaten the World Economy" (Princeton University, $26.95), Raghuram G. Rajan concludes that the financial crisis erupted "because in an integrated economy and in an integrated world, what is best for the individual actor or institution is not always best for the system."

Like geological fault lines, the fissures in the world economic system are more hidden and widespread than many realize, he says. And they are potentially more destructive than other, more obvious culprits, like greedy bankers, sleepy regulators and irresponsible borrowers.

Mr. Rajan, a finance professor at the University of Chicago and former chief economist at the International Monetary Fund, argues that the actions of these players (and others) unfolded on a larger worldwide stage, that was (and is) subject to the imperatives of political economies.

He cites three fault lines: domestic political stresses; trade imbalances among countries; and the tensions produced when financial systems with very different structures interact. All three came together to damage the financial sector in 2008, he says, and could meet again to cause another crisis.

Continue reading "Fault Lines: How Hidden Fractures Still Threaten the World Economy" »

Nevertheless, JPMorgan agreed to sell the loan to Inbursa on July 15, 2009, court documents show. It did not inform Cablevision and went ahead with the deal despite the fact that Grupo Televisa and other banks were interested in purchasing part of the loan.

When it sold the loan to Inbursa, JPMorgan structured it as a participation agreement rather than an assignment; such agreements can be sold without the borrower's consent. Still, the terms of the original Cablevision loan stated that participations could be sold only if the lending relationship between JPMorgan and Cablevision did not change significantly. Cablevision argued that the transaction with Inbursa did just that.

Cablevision learned that the sale to Inbursa required JPMorgan to hand over virtually any information Inbursa wanted about Cablevision. Court documents show that this language was added to the agreement at Inbursa's request.

Since the princes are nicer and more impressive, it is easy to be seduced into the belief that they also are more trustworthy. This is false. During the last few years, for example, the princes at Citigroup, Bear Stearns, Goldman Sachs and Lehman Brothers behaved with incredible stupidity while the hedge fund loners often behaved with impressive restraint.

As Sebastian Mallaby shows in his superb book, "More Money Than God", the smooth operators at the big banks were playing with other people's money, so they borrowed up to 30 times their investors' capital. The hedge fund guys usually had their own money in their fund, so they typically borrowed only one or two times their capital.

The social butterflies at the banks got swept up in the popular enthusiasms. The contrarians at the hedge funds made money betting against them. The well-connected bankers knew they'd get bailed out if anything went wrong. The solitary hedge fund guys knew they were on their own and regarded their trades with paranoid anxiety.

Updated tables tracking federal financial reform.

For decades an order to buy or sell a security went to a person in a trader's jacket standing on the floor of an exchange, often at the NYSE in Lower Manhattan. If you wanted to sell stock in General Electric, for instance, these so-called specialists would find a buyer. If they couldn't find one, they bought it themselves.

In exchange for their services, the specialists pocketed some of the difference between the price at which you were willing to buy and the price at which a GE holder was willing to sell.

This system came under attack in the early 1980s from Nasdaq, a rival marketplace for stocks, which began using computers to make trades. The pitch was it could match buyers and sellers faster than humans, and for less money.

Then, starting in the late '90s, the NYSE specialists got hit again, this time with a series of blows: new rules encouraging computer matching of buyers and sellers, a shift to quote stock prices in minute increments of decimals instead of fractions, and a decision to cut the minimum spread that specialists or other middlemen could grab for themselves from 6.25 cents per share to a penny.

''It used to be an oligopoly, an old boy's club,'' said Irene Aldridge, head of an HFT shop called Able Alpha Trading and author of ''High-Frequency Trading.'' ''But now it's a completely level field.''

Critics of high-frequency trading say all this talk about narrowing spreads for ordinary investors distracts from a key problem: Split-second trading without human supervision is a recipe for disaster

Continue reading "High Frequency Traders (HFT) Driven by Spread Squeeze" »

FBI fraud alert for mortgage.

Akerlof and Romer (1994)? They show that the common thread in many financial crises is "looting", i.e., fraud. Reading their paper, it is clear that the current crisis was utterly predictable. The Wall Street "banksters" make the street gangs you refer to look like a bunch of pikers.

Looting: The Economic Underworld of Bankruptcy for Profit

George A. Akerlof

University of California, Berkeley; National Bureau of Economic Research (NBER)

Paul M. Romer

Stanford Graduate School of Business; National Bureau of Economic Research (NBER)

April 1994

NBER Working Paper No. R1869

Abstract:

During the 1980s, a number of unusual financial crises occurred. In Chile, for example, the financial sector collapsed, leaving the government with responsibility for extensive foreign debts. In the United States, large numbers of government-insured savings and loans became insolvent - and the government picked up the tab. In Dallas, Texas, real estate prices and construction continued to boom even after vacancies had skyrocketed, and the suffered a dramatic collapse. Also in the United States, the junk bond market, which fueled the takeover wave, had a similar boom and bust.

In this paper, we use simple theory and direct evidence to highlight a common thread that runs through these four episodes. The theory suggests that this common thread may be relevant to other cases in which countries took on excessive foreign debt, governments had to bail out insolvent financial institutions, real estate prices increased dramatically and then fell, or new financial markets experienced a boom and bust. We describe the evidence, however, only for the cases of financial crisis in Chile, the thrift crisis in the United States, Dallas real estate and thrifts, and junk bonds.

Our theoretical analysis shows that an economic underground can come to life if firms have an incentive to go broke for profit at society's expense (to loot) instead of to go for broke (to gamble on success). Bankruptcy for profit will occur if poor accounting, lax regulation, or low penalties for abuse give owners an incentive to pay themselves more than their firms are worth and then default on their debt obligations.

A theory of Aaron Fine, a partner and consumer banking specialist with the consulting firm Oliver Wyman. He argues that more affluent customers have suddenly become a lot more valuable to the banks.

Why? Well, a big chunk of the fee income from the more stretched classes of bank customers stands to go away because many of those people will opt out of paying fees to overspend.

"I expect you'll see another wave of innovation coming from the banks," he said. "And perhaps the first segment they'll address is the higher balance accounts."

Continue reading "Ideal customer according to Oliver Wyman" »

Shelby, the ranking Republican on the Senate Banking Committee, has already signaled that he'll fight the Obama administration's push for a "Volcker rule" to rein in too-big-to-fail financial behemoths. The conservative message guru Frank Luntz has drafted a memo instructing G.O.P. legislators on how to defeat a new Consumer Financial Protection Agency while camouflaging themselves as populist foes of the very banks and credit card companies that that agency would regulate. That's a neat trick -- Luntz's nonpolitical clients include Merrill Lynch and American Express -- and it helps explain why Wall Street is now tilting its contributions to Congressional Republicans for 2010.

![Reblog this post [with Zemanta]](http://img.zemanta.com/reblog_e.png?x-id=491a5982-1e93-4a7a-95f8-14ac46f0bb21)

Continue reading "Shelby, Senate Banking Committee vs Volcker rule" »

a bubble is a form of psychological malfunction. And like mental illness there's a tricky gray area between being really sick and just having a few problems, Mr. Shiller said during a panel discussion at the World Economic Forum in Davos, Switzerland.

The solution: a checklist like psychologists use to determine if someone is suffering from, say, depression. So here is Mr. Shiller's checklist.

Figures released this week by the Federal Reserve showed that Americans owed $10.8 trillion on home mortgages at the end of the third quarter, down 2.2 percent from a year earlier and the lowest level since mid-2007.

Similarly, the Fed said that outstanding credit card bills in October totaled $888 billion, down 8.5 percent from a year earlier. That number was the lowest since March 2007.

Those trends do not, however, necessarily indicate that Americans have paid down their debts and are starting to lead the more frugal lives that some financial planners have been recommending for years. There has undoubtedly been some of that, but the declines also indicate that banks have been forced to write off a lot of bad debts and have grown more stingy in granting credit.

As can be seen from the accompanying charts, banks' credit card write-offs have soared, to an annual rate of 10.2 percent in the third quarter of this year.

And the Mortgage Bankers Association reported that at the end of the third quarter, 4.5 percent of all mortgages were in foreclosure -- one in 22 mortgages. It said another 6.1 percent -- one in 16 -- were at least two months overdue. Those figures are for all mortgages, not just subprime ones.

The for-profit higher education sector is no stranger to scandal. In the 1980s and early '90s, it came to light that hundreds of fly-by-night schools had been set up solely to reap profits from the federal student loan programs, in part by preying on poor people and minorities. The most unscrupulous of them enrolled people straight off the welfare lines, and got them to sign up for the maximum amount of federal student loans available--sometimes without their knowledge or consent.

The rampant abuses caught the attention of the news media, sent shockwaves through Capitol Hill, and led to a year-long, high-profile Senate investigation led by Senator Sam Nunn, the Georgia Democrat. The standing-room-only hearings had all the trappings of scandal, with trade school officials pleading the Fifth and a school owner, who had been convicted of defrauding the government, brought to the witness table in handcuffs and leg irons.

Key lawmakers considered kicking all trade schools out of the federal student aid programs--a virtual death sentence given the institutions' heavy reliance on these funds. But Congress ultimately stepped back from the brink and instead strengthened the Department of Education's authority to weed out problem institutions. Under the new rules, for-profit colleges had to get at least 15 percent of their tuition money from sources other than federal loans and financial aid. Also, if more than a quarter of a school's students consistently defaulted on their loans within two years of graduating or dropping out, the school could be barred from participating in federal financial aid programs. The idea was to get rid of those schools that were set up solely to feed on federal funds and didn't provide the meaningful training students needed to get jobs and pay off their debt. As a result, during the 1990s more than 1,500 proprietary schools were either kicked out of the government's financial aid programs altogether or withdrew voluntarily. In an effort to rein in abusive recruiting tactics, in 1992 Congress also barred schools from compensating recruiters based on the number of students they brought in.

These changes shook up the industry. The old generation of trade schools gradually died off and were replaced by a new breed of for-profit colleges--mostly huge, publicly traded corporations. The largest, the Apollo Group, owns the University of Phoenix, which serves more than 400,000 students at some ninety campuses and 150 learning centers worldwide. Others include the Career Education Corporation, which serves 90,000 students at seventy-five campuses around the world, and Corinthian Colleges, which serves 69,000 students at more than 100 colleges in the United States and Canada.

Not only did these companies promise that their schools would be more responsive to the needs of students and employers than the previous generation, they also said they would be more accountable to the public because, as publicly traded companies, they were heavily regulated. "We've seen a fire across the prairie, and that fire has had a purifying effect," Omer Waddles, then the president of the Career College Association, told the Chronicle of Higher Education in 1997. "As our sector has weathered the storms of recent years, a stronger group of schools is emerging to carry, at a high level of credibility, the mantle of training and career development."

In reality, the new breed of schools had quite a bit in common with their predecessors; in some cases, they even operated out of the same buildings and employed the same personnel. What's more, rather than making them more accountable, the fact that they were publicly traded created a powerful incentive for them to game the system. After all, to keep their stock prices up and investors happy, the schools had to show that they were constantly expanding, which meant there was intense pressure to get students in the door and signed up for classes and financial aid.

Continue reading "Private schools, private loans, not all exclusive and elusive" »

MSNBC: In hindsight was Paulson right? If Congress did not write that $700 billion check would banks have collapsed?

Warren: I have to say I think there would have been some real pain. There are some businesses today that are alive that would have been wiped out. However, I am just not convinced at all that we would have gone into a death spiral"

MSNBC: With the facts he knew at the time, was it the right call?

Warren: (struggling to be polite) "You know, let me say it this way. The question about whether or not the world as we know it has ended, depends on what you think the world is as we know it. If you think the world as we know it, are a handful of huge financial institutions, the dinosaurs that roamed the earth, then you're right. They are not going to exist without huge infusions of government money. On the other hand if what you really believe is that our economy and our world is 115 million American households you start to see it very differently. And you say, you know if the dinosaurs are gone there are still a lot of stuff to be done.

Visit msnbc.com for Breaking News, World News, and News about the Economy

The popularity of the term "green shoots" shows the kind of social epidemic underlying our changing thinking. The phrase was propelled in Britain by Shriti Vadera, the business minister, in January, and mutated into a more contagious form after Ben Bernanke, the Federal Reserve chairman, used it on "60 Minutes" on March 15.

The news media didn't need to change the term for different cultures around the world. With nothing more than a quick translation -- brotes verdes, pousses vertes, grüne Sprösslinge, etc. -- it is now recognized as a symbol of a revival coming soon.

All of this suggests that a social epidemic is supporting renewed confidence. This confidence can keep growing by contagion, as a kind of self-fulfilling prophecy, and we may see the markets and the economy recover further.

The traumatic upheaval that has roiled Wall Street during the past two years has produced - surprisingly quickly - a widely acknowledged new pecking order in the world of high finance: Goldman Sachs, in trading, and JPMorgan Chase, in banking, have become the undisputed industry leaders, with a hand in nearly every deal or trade. Clients can try to avoid these two, but only at their own peril.

The likes of Morgan Stanley, Barclays and Bank of America/Merrill Lynch - wounded but not fatally - continue to seek a firm footing on which to operate, while the so-called "zombie banks", such as Citigroup and Wells Fargo, remain on life support. Boutiques, such as Lazard, Greenhill, Rothschild, Evercore and Jefferies, that primarily provide advice to clients - and little capital - have been hiring broadly and have seen a resurgence of activity in their restructuring businesses, where a wave of recapitalisation and "amend and extend" deals have allowed many overleveraged companies to avoid bankruptcy filings. For the boutiques, the question remains whether, any time soon, there will be enough non-restructuring advisory business - formerly known as M&A - to justify all the new hiring.

But none of this is particularly surprising in the wake of the worst crisis to hit banking since the Great Depression produced the Glass-Steagall Act and the separation of investment banking from commercial banking.

What does seem to be spooking Wall Street these days, though, is the traction that some private equity firms, such as KKR and Apollo Advisors, and hedge funds, such as Citadel Investment Group, appear to be "backward integrating" into investment banking by building up their businesses that compete with Wall Street in the lucrative underwriting of debt and equity securities.

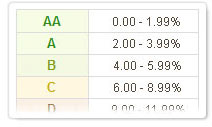

Credit rating mapped to loss rate by score band using a credit model.

Prosper comes back to life, with SEC filing.

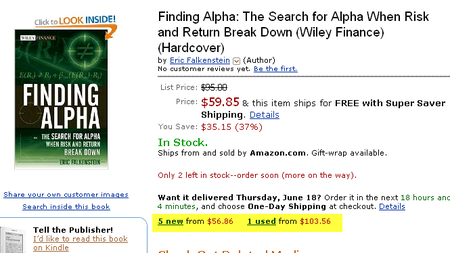

Finding Alpha: The Search for Alpha When Risk and Return Break Down (Wiley Finance) by Eric Falkenstein (Hardcover - Jun 29, 2009) is anticipated and now available.

The typical Amazon new vs used arbitrage occurs. New $56, vs used $103.

See previously Big Picture Barry Bailout Nation arbitrage.

Bernanke speaks:

1. How Did We Get Here? What caused our financial and economic system to break down to the extent it has?

2. What Is the Fed Doing to Address the Situation?

3. Does the Fed's Aggressive Response Risk Inflation Down the Road? Could the Fed's aggressive actions to stabilize the economy today lead to an inflation problem down the road?

4. Why Did the Fed and the Treasury Act to Prevent the Bankruptcy of Some Major Financial Firms? Why did the Fed and the Treasury act to prevent the bankruptcy of some major financial firms, such as the investment bank Bear Stearns and the insurance company American International Group, or AIG?

Continue reading "Bernanke: 4 questions (and 4 answers) on economic crisis" »

For years, managing a hedge fund, and making a fortune for yourself in the process, was the running dream on Wall Street. But now that industry, like much of finance, is withering. Many hedge fund investors are folding. Since last May, these funds' assets under management have dwindled to $964 billion from $1.4 trillion. The private equity business, one of the iconic businesses of the boom, is struggling with a deep slump of its own.

Most large banks have over $US 1 trillion assets under management.

Continue reading "Hedge funds industry shrinks to under $ trillion " »